Econometrics is a field of economics that uses statistical methods to analyze and model economic data. It is beneficial for understanding relationships between variables, testing economic theories, and making predictions. In this article, we will explore some fundamental concepts of econometrics regression analysis, co-integration, Granger causality, and hypothesis testing along with their assumptions, mathematical equations, and real-world applications, particularly in market data analysis and predictive modelling.

|

| Created with AI |

Regression Analysis: A Fundamental Tool in Econometrics

Regression analysis is the backbone of econometrics, it helps us understand how one variable influences another (Nothing but a cause and effect). It models relationships between a dependent variable and one or more independent variables. The simplest form of regression analysis is simple linear regression, which models the relationship between two variables. For example, we can examine how a company’s sales (dependent variable = "Y") depend on advertising expenditure (independent variable = "X").

The equation for simple linear regression is:

Where:

- is the dependent variable (e.g., sales).

- is the independent variable (e.g., advertising expenditure).

- is the intercept (constant).

- is the slope coefficient (the change in for a unit change in ).

- is the error term (captures unobserved factors).

Assumptions in Regression Analysis:

- Stationarity: A flat-looking series, without trend, constant variance over time, and a constant autocorrelation structure over time. This assumption needs to be checked for the dependent variable and residual of the model.

- Linearity: The relationship between the dependent and independent variables should be linear.

- Multicollinearity: The independent variables should be independent of each other.

- Autocorrelation: The observations of the series should be independent of each other.

- Homoscedasticity: The variance of errors should be constant across all of the independent variables.

- Normality: The errors are normally distributed.

2. Co-Integration: Modeling Long-Term Relationships

Co-integration is used when we want to understand long-term relationships between non-stationary variables. Non-stationary variables have trends over time, which could lead to misleading results in traditional regression analysis. Co-integration helps identify whether two or more series are related in the long run, even if their individual trends are not stationary.

Mathematical Model for Co-integration:

Let’s say we have two-time series variables, and . If both are non-stationary but their linear combination βis stationary, then and are said to be co-integrated.

This means that and move together in the long-run equilibrium, even though they may exhibit short-term fluctuations. The parameter represents the long-term equilibrium relationship between the variables.

Assumptions in Co-integration:

- Both series should be non-stationary but of the same order of integration.

- The linear combination of the variables should be stationary.

3. Granger Causality: Exploring Causal Relationships

Granger causality is used to determine whether one time series can predict another. It does not necessarily imply a direct cause-and-effect relationship but rather a predictive relationship. If a time series Granger causes , it means that past values of help forecast future values of .

Granger Causality Equation:

The Granger causality test typically involves checking if lagged values of one variable (say, ) help predict the current value of another variable (say, ).

Where:

- is the dependent variable (e.g., stock prices).

- represents the lagged values of the independent variable (e.g., interest rates).

- is a constant.

- and are coefficients that capture the influence of past values of and , respectively.

If the coefficients are significantly different from zero, we conclude that Granger causes .

Assumptions in Granger Causality:

- The time series must be stationary, or made stationary by using any transformation like log, differencing, etc...

- The appropriate lag length should be chosen to avoid model overfitting or underfitting.

4. Hypothesis Testing: Making Decisions Based on Data

Hypothesis testing is crucial in econometrics as it helps us test assumptions or theories about economic relationships. It involves two hypotheses:

- Null Hypothesis (H0): The assumption we want to test (usually that there is no effect).

- Alternative Hypothesis (H1): The opposite of the null hypothesis (usually that there is an effect).

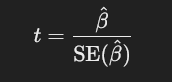

Example: in regression analysis, a common hypothesis is that the slope coefficient () is zero, meaning no relationship between the variables. We use statistical tests like the t-test or F-test to test these hypotheses.

Mathematical Representation:

1. t-test: Tests whether a regression coefficient is significantly different from zero.

- is the estimated coefficient.

- is the standard error of the coefficient.

- are the residual sum of squares for the restricted and unrestricted models.

- is the number of restrictions.

- is the number of observations.

- is the number of parameters.

Assumptions in Hypothesis Testing:

- The data should be randomly sampled.

- The errors should be independent and identically distributed.

5. Applications in Market Data and Predictive Modeling

Econometrics is widely used in analyzing market data to create predictive models. For example:

- Predicting Stock Prices: Regression models can predict future stock prices based on historical data and various predictors such as interest rates, economic indicators, or company performance.

- Forecasting Demand: Businesses can use econometric models to forecast demand for products or services based on past sales data and market conditions.

- Monetary Policy: Econometric models help policymakers predict the impact of interest rate changes on inflation and economic growth.

Recommended Courses for Learning Econometrics:

- Coursera: Econometrics: Methods and Applications – A comprehensive course that covers regression analysis, hypothesis testing, and other key econometric techniques.

- Udemy: Econometrics for Beginners – A beginner-friendly course focusing on the core principles of econometrics and practical applications.

- edX: Introduction to Econometrics – A course offered by top universities that provides a solid foundation in econometric methods, with real-world examples.

Conclusion:

Econometrics is a powerful tool for analyzing market data, testing economic theories, and building predictive models. By mastering concepts like regression analysis, co-integration, Granger causality, and hypothesis testing, one can make informed decisions, whether in business, finance, or policymaking. To become proficient in econometrics, it is crucial to understand both the underlying assumptions and the mathematical techniques involved. With the right training and application, econometrics can help unlock valuable insights and predict future trends in the market.